SpaceX's first full public trading day produced a price, not a business audit. The paper's June 12 story said the first trade priced Starlink, xAI hopes, Mars optionality, and Musk control together. CNBC now gives the numbers: a $135 IPO price, a $150 open, a $176.52 intraday high, a $160.95 close, and $166.85 after hours. [1] [2]

Those numbers are impressive. They are also easy to overread. A first-day premium proves that buyers wanted scarce SpaceX stock more than sellers wanted to part with it. It does not prove Starlink margins, Mars economics, free cash flow, xAI adjacency, or governance durability under Elon Musk.

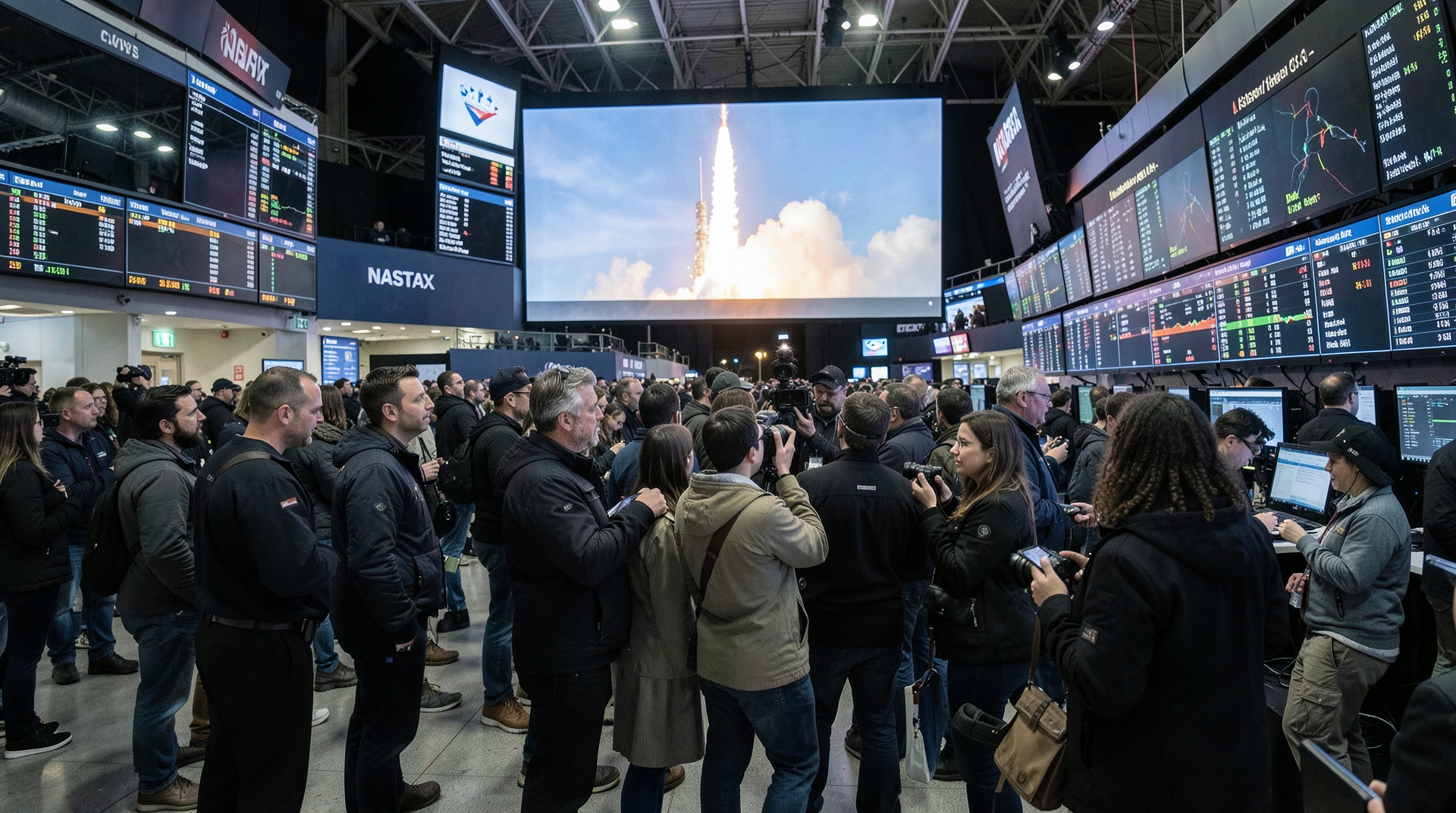

CNBC's day-one account quotes investor reaction around demand, scarcity, and the quality of the debut. [1] Its live IPO coverage preserves the opening sequence and the ceremony of a market event that had been anticipated for years. [2] A separate CNBC market wrap says SpaceX's successful debut relieved a week of broader market anxiety about mega-IPO supply, with OpenAI and Anthropic waiting in the pipeline. [3]

That last point is the more interesting one. SpaceX is not only a rocket company entering the public market. It shows how much public equity can absorb from the private mega-cap stack. If one huge debut trades well, bankers can argue the window is open. If it trades only because the float is scarce, the lesson is narrower.

The X frame turns the same price record into biography. Musk loyalists see public vindication. Skeptics see retail appetite for a mythic valuation. Traders see a first-day structure. None of those readings is wrong enough to ignore, but none substitutes for the income statement that public investors still need.

The unanswered operating question is Starlink. SpaceX's valuation depends on the satellite business becoming more than a launch halo. Investors need churn, average revenue, capex, launch cadence, terminal costs, regulatory exposure, and cash conversion. A rocket image can open a trading day. It cannot explain a multiple.

The public price changes the incentive for disclosure. As long as SpaceX was a private trophy asset, the valuation could travel through secondary sales, fund marks, mythology, and scarcity. Public trading asks the company to survive comparison. Investors will compare it with defense contractors, telecom carriers, satellite operators, AI infrastructure names, and every other company that claims a future large enough to excuse present spending.

CNBC's market wrap is useful because it shows the SpaceX debut influencing the supply conversation beyond SpaceX. [3] A successful trade can reopen the road for other enormous offerings. It can also drain attention and capital from the same investors who are being asked to buy OpenAI, Anthropic, cloud infrastructure, and whatever comes after. The market did not only price a company. It priced an issuance window.

Governance is the quiet premium or discount. Musk's control can be treated as founder genius, brand concentration, key-person risk, political volatility, or all four at once. A strong first day does not resolve which one public investors bought. It only shows that on day one enough of them accepted the package.

Mars is the other line item that refuses to stay in a line. It is mission, recruiting tool, political project, brand asset, and capital sink. A public market can pay for optionality, but it will eventually ask whether optionality consumes cash faster than Starlink produces it.

The first close above the IPO price gives bulls the better opening argument. [1] The after-hours price gives them an even cleaner weekend headline. [1] But the paper should resist making one trading day do a decade of financial work. Day one is evidence of demand for shares. It is not evidence that the Mars program funds itself, that Starlink margins hold, or that xAI adjacency increases rather than confuses the equity story.

The first close therefore settles one question and opens three. Demand was real on day one. The market did not reject the Musk premium. And the next wave of AI and space supply now has a precedent to cite. What it does not settle is whether the valuation rests on operating cash, strategic scarcity, or the willingness of public investors to buy a private-market legend at public-market scale.

The sober conclusion is strong but limited. SpaceX stuck the landing in the market. Now the market gets to ask what, exactly, landed.

-- THEO KAPLAN, San Francisco