TL;DR

Seven insurance mutuals withdrew war risk cover for the Persian Gulf, and every container arriving at your port now costs thousands more — the war tax nobody voted for.

MSM Perspective

Reuters led with the premium surge numbers; Bloomberg broke the seven-club cancellation; Al Jazeera connected the dots to consumer energy costs.

X Perspective

Shipping and finance X is circulating the P&I club cancellation notices like they're classified documents — the spreadsheet that closed the Strait of Hormuz.

On March 1, 2026, five of the world's largest Protection and Indemnity clubs — Gard, Skuld, NorthStandard, the London P&I Club, and the American Club — issued formal notices of cancellation for war risk coverage in the Persian Gulf, Iranian territorial waters, and adjacent sea areas. [1] The notices gave 72 hours. At midnight GMT on March 5, the coverage terminated automatically. [2] Two additional clubs followed within days. The Strait of Hormuz was not closed by a navy. It was closed by an actuary.

A supertanker valued at $250 million cannot sail without hull and machinery insurance. Its cargo cannot be financed without cargo insurance. Its crew cannot be contracted without P&I liability cover. When the insurers withdrew, the ships stopped. More than 150 vessels were stranded in the first week. [3]

The Insurance Chain

The architecture is layered and invisible. P&I clubs are mutual insurance associations owned by their shipowner members, collectively covering roughly 90 percent of the world's ocean-going tonnage. [4] Above them sit reinsurers. The cancellation notices did not originate with the clubs. They originated with the reinsurers, who informed the clubs that war risk coverage for the Persian Gulf could no longer be underwritten at any price consistent with solvency requirements. [1] The clubs passed the cancellation to their members. The members pulled their ships.

Gard explained the decision in clinical terms: it had "received Notice of Cancellation from its reinsurers in respect of war risks in Iran and Persian/Arabian Gulf waters." [1] Skuld and NorthStandard issued nearly identical language. [5] [6] When the reinsurance market decides a risk is uninsurable, the decision propagates through the system in hours.

Before the war, a standard war risk premium for a tanker transiting the strait ran at roughly 0.05 percent of hull value — perhaps $125,000 for a single VLCC transit. [7] By March 6, Reuters reported the new rate had reached 3 percent of hull value. [7] For a supertanker valued at $250 million, that is $7.5 million per transit. Marsh estimated near-term hull rate increases of 25 to 50 percent even for vessels outside the immediate conflict zone. [8]

The Surcharge Cascade

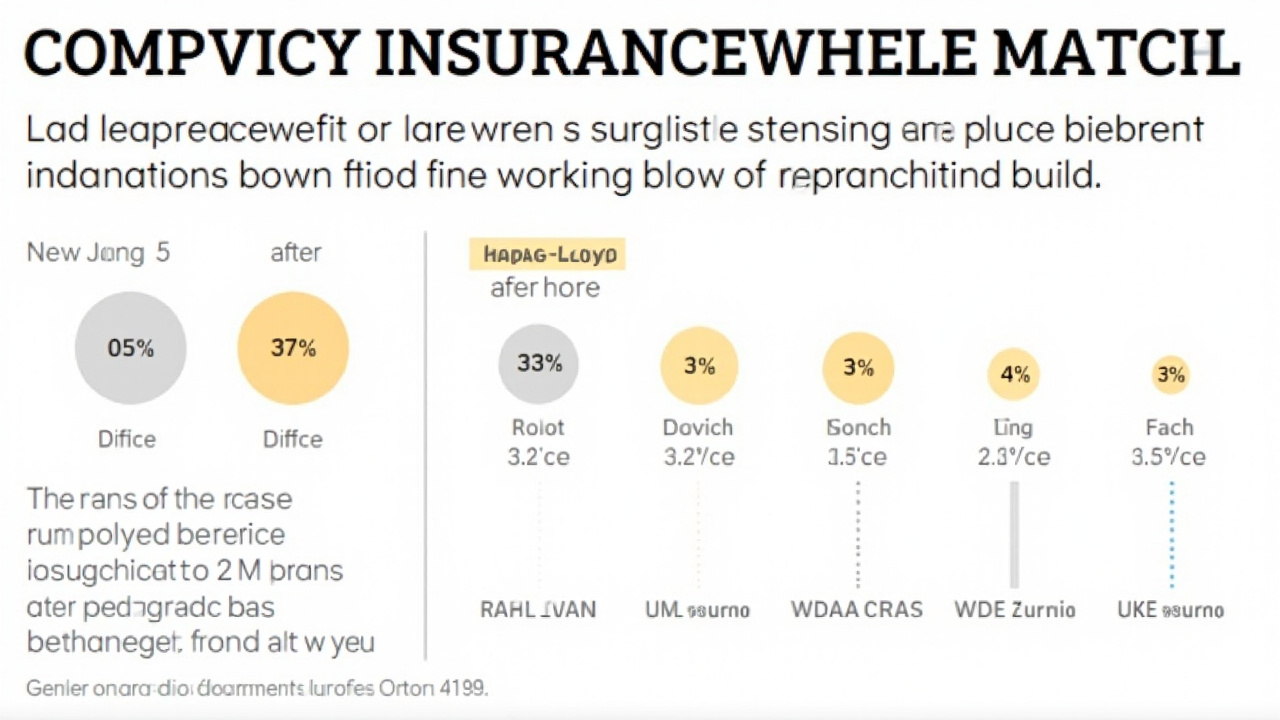

Insurance is a cost. Costs are passed through. On March 2, Hapag-Lloyd, the world's fifth-largest container shipping line, imposed a War Risk Surcharge of $1,500 per twenty-foot equivalent unit for standard containers and $3,500 per container for refrigerated and special equipment. [9] The surcharge applied to every booking issued on or after that date for cargo to or from the Upper Gulf, Arabian Gulf, and Persian Gulf. [10] CMA CGM, the world's third-largest line, followed with an emergency conflict surcharge of $2,000 per twenty-foot dry container, $3,000 per forty-foot container, and $4,000 per reefer or special equipment. [11] Maersk, the world's second-largest, suspended Gulf bookings entirely. [12]

A single forty-foot container of consumer electronics from East Asia to the Gulf now carries $3,000 to $4,000 in war surcharges alone — before the base freight rate, fuel surcharges, and terminal handling charges that preceded the war. SP Global reported that tanker freight rates had spiked to record levels, with most commercial tankers now avoiding the Strait of Hormuz entirely. [13] Rerouting via the Cape of Good Hope adds 10 to 14 days to Europe-bound voyages. Every additional day at sea burns fuel, ties up capacity, and compounds the scarcity the market is trying to price.

Who Pays

The surcharge propagates through every supply chain that touches oil, petrochemicals, plastics, fertilizers, or manufactured goods that transit the world's busiest energy corridor. No price tag says "war risk surcharge included." No gas station receipt itemizes the insurance premium embedded in the crude. The cost arrives as inflation — in goods, in shipping, in the figures that central banks watch and cannot control.

Fitch Ratings described the withdrawal as "credit negative for exposed U.S. marine insurers," warning of reserve adequacy concerns and potential downgrades. [14] CNBC reported that premiums will continue rising for the duration of the conflict. [15] Trump signed an executive order on March 4 directing the Development Finance Corporation to offer political risk insurance as a government backstop. [16] The order acknowledged what the market had decided: the private insurance industry will not underwrite the Persian Gulf at any viable price. The government is proposing to insure the risk of its own war.

The Arithmetic

The numbers compose a simple picture. Seven P&I clubs covering 90 percent of global tonnage withdrew war risk cover. [1] Lloyd's war risk premiums rose over 1,000 percent. [4] Container surcharges of $1,500 to $4,000 per box were imposed by every major carrier. [9] [11] Tanker transit through the strait dropped from roughly 50 vessels per day to near zero. [3] Rerouting via the Cape added $800,000 to $1 million in fuel costs per voyage for a laden VLCC. [7]

None of these numbers appear in the war's casualty figures. None are discussed in the Pentagon's briefings. None feature in the administration's narrative of "Operation Epic Fury." They are the war's invisible tax — assessed by actuaries, collected by carriers, paid by everyone who buys anything that once moved through the Persian Gulf. The insurance industry did not choose a side. It did what insurance industries do: it measured the risk, found it unmeasurable, and withdrew. The strait closed itself, not with a blockade but with a cancellation notice.

-- PRIYA SHARMA, Delhi

Sources & X Posts

News Sources

X Posts